Did you have a piggy bank while growing up? The one in which you could put in small monies given as gifts by your favourite aunts and uncles on festival days. When you were the topper of your class in an examination, your proud father would give you a small reward, and you would cherish it, save it. These small savings in the piggy bank would one day come in handy to buy something precious, with your own money!

The habit of saving is one of the first golden rules of money management. Money saved is money earned. Not everybody can get massive pay hikes year on year. However, getting a 10% pay hike and setting aside 10% of your existing income as savings, both have the same effect on your finances. Getting a super hike is not entirely in your hands, but saving is something that you can do. So take the first step now. Start saving in small quantities, you might find the pointers given below useful to cultivate the saving habit.

Do small savings matter?

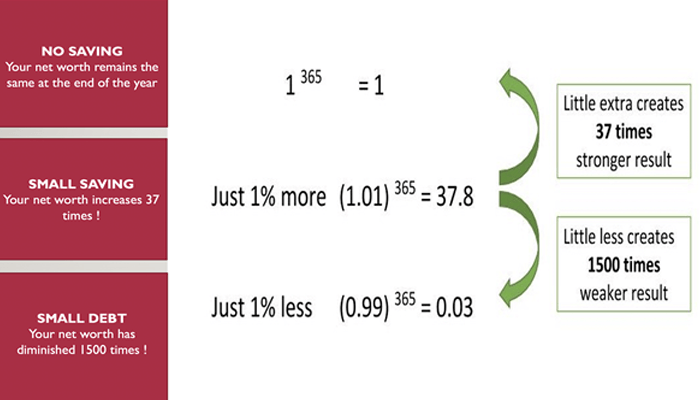

Simple straight answer. Yes, they matter very much. There is a popular mathematical principle that can be quoted as reference to highlight the importance of small savings.

The picture is referring to a daily saving cycle. But you can relate to it better when you consider small savings made every month. As opposed to not saving at all. The reason is obvious – the small incremental saving will compound in value over a period of time. So your principal will increase substantially at the end of the tenure.

There is a major hidden benefit that comes with cultivating the habit of saving. It is the critically important characteristic of self-denial and financial discipline. When you learn to say NO to some unnecessary/avoidable expense and save the money instead, that’s a big step towards personal growth and maturity.

Different types of small savings

There are 3 primary routes in which investors can plough in their small savings over regular periods of time. Most of them are monthly installment schemes, some have a yearly cycle

1.Government Small saving schemes

This is the most popular investment option among Indian citizens. The Government of India has several schemes that involve small monthly/yearly contributions such as PPF, Sukanya Samruddhi Yojana, Post Office Recurring Deposits and so on. These schemes come with the added benefit of Income Tax Deduction upto an amount of Rs 150000 under Section 80C. These schemes offer reasonable rates of interest anywhere between 5.5-7.5%. The most important aspect is their absolute guarantee of safety as they are Central Government schemes.

The downside to this investment route is the continuously dropping interest rates, and thus the returns are bound to be less attractive with passing years. And the lack of liquidity of your funds as they are locked in the schemes for fixed durations.

2.Systematic Investment Plans (SIP) for Mutual Funds

Its always difficult to decide when to enter the stock markets, whether to do it when the markets are buzzing upward or when they are on a downward spiral. The best way to balance out your risks of equity investments is to enter the market through the SIP route. The MF scheme of your choice will keep accumulating MF units in small quantities every month, depending on the quantum of your SIP installment. When you want to get your money back, you can sell just the required number of units at the prevailing market rates. MFs from reliable fund houses are known to generate around 8-14% returns in the markets depending on the prevailing market conditions. However, the biggest disadvantage with the stock market is the inherent risk involved. There is no guarantee of returns and your investment is subject to market risk.

3.Chit Funds

Many of you may not realize but Chits Funds operate in the same small savings model. They are actually an instrument of regular monthly savings with the added advantage that the depositor can withdraw their entire investment at the time of their need, any time during the investment tenure. No penalties, no hassles.

Choose a registered Chit fund house that has a long standing reputation and you can expect to gain about 7-9% returns on your investment with absolutely no risk.

ABOUT US

Shanthala Chits has been in the business of chit funds for over 2 decades now. We are a Government approved chit fund company with a 28 year successful track record and thousands of satisfied customers. Shanthala Chits is registered under the Chit Fund Act of 1982, Government of Karnataka. We are one of the most popular chit fund houses based out of Bengaluru, known for our customer satisfaction and secure investments.

Our Chit schemes range from a monthly contribution of Rs 8,000 to Rs 1,00,000 to suit every budget. You can pick a chit scheme with an appropriate monthly installment for meeting several of your short-term financial needs. Our chit schemes are for a tenure of 25 Months.

Get in touch with us and start with an investment scheme. We will be glad to help you out with the right scheme that matches your needs.

- How to use Chit Funds to raise capital for your business - March 25, 2025

- 5 SIMPLE MANTRAS TO ACHIEVE FINANCIAL FREEDOM - December 26, 2024

- HOW CAN CHIT FUNDS HELP BUSINESS OWNERS AND START-UPS? - October 26, 2024