In the earlier blog, we highlighted some of the solutions that chit funds provide to people interested in engaging in an easy mode of savings as well as borrowings.

But the question that many often ask is how safe it is to park your money in a privately-owned chit fund?

True, this is a question that is worth asking given that a potential customer would put his or her hard-earned money at the hands of someone whom they hardly know. Despite chit funds being active in India for decades now, some incidents of fraud have made a section of potential customers of the financial instrument weary and even skeptical.

Therefore, it is important that those who are interested in making investments in chit funds or even those who are not – including young salaried people and professionals, should get some assurance about the stability and viability of chit funds in Indian and some security about the safety and security for their hard-earned money.

The first and the most important suggestion that financial experts give to such individuals is to ensure that they make an informed choice about the chit fund company that they would want to invest in.

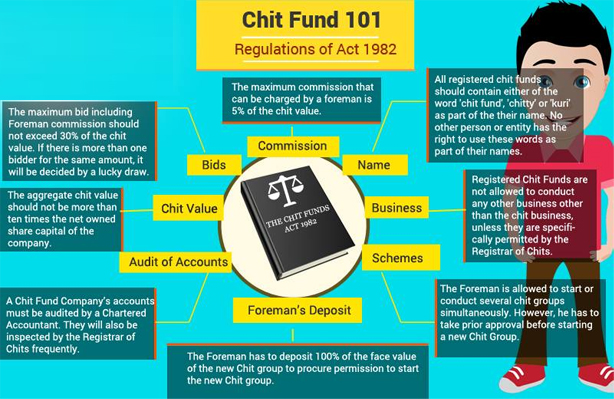

Before investing in any chit fund, a potential investor should make sure that the company runs chits according to the established regulations – some made by the central government and others by the state governments. Mostly, the Chit Fund Act 1982 of the government of India should ideally be governing the Chit funds. The regulations are implemented by the Registrar of Chits and any chit fund such as Shanthala chits which are closely monitored by this regulatory body can assure safety and security of the money parked with them. Under the regulations, every chit company needs to deposit the aggregate value of each chit scheme with the Registrar of Chits which ensures that in case of any default by the chit company, the investors can be assured to get back their money, according to says Sridhar Alampalli, promoter of Shanthala Chits.

But yet the question might linger as to why anyone would choose to invest in chit funds instead of the established banking system.

We have elaborated the scope for obtaining easy loans from chit funds in the earlier blog. But that is not all. There are other reasons that one can support one’s decision for investing in chits – those that are hardly provided by the established banking system.

For one, the habit of making small monthly but regular investments creates a sense of financial discipline. The habit of keeping away investment decision for tomorrow is common in a lot of people. Further, there are many who are only able to save money if they are forced to – for example via auto debit for a money back life insurance policy. And this trend can be more prevalent among the young salaried people and professionals (MILLENNIAL GENERATION – BORN 1981-1996) who like to live in the ‘Today’ and believe ‘Tomorrow’ is far off. Therefore, making small but regular investments in chit funds creates the much-needed habit of saving for tomorrow’s needs and instills a form of financial discipline.

Most chit funds have a unique way of fixing the rates of interest on borrowings where the participants themselves decide on the rate and not an external agency. This means that the rates tend to be much lower than what would be charged for a personal loan. Further, the intermediation cost is the lowest when compared to other financial instruments. These are elements of chit funds that one can hardly find with any traditional banks.

Therefore, chit funds offer more than one financial solution. And while the older – and arguably the wiser, can be assumed to already possess knowledge about various aspects of personal finance, investing in chit funds can be a very good learning experience for the younger generation in a practical way.

Therefore, it can be concluded that while a careful selection of a chit fund can ensure the safety of your money, investing in such firms can also help you develop certain habits that are not offered by any traditional banks.

- TAKE SMALL STEPS TOWARDS FULFILLING YOUR DREAMS - November 21, 2024

- Learn how to detect safe chit funds - November 14, 2024

- GIVE A FRESH START TO YOUR PERSONAL FINANCES THIS DUSSEHRA - October 19, 2024

The efficacy of antibiotic prophylaxis has been demonstrated to be significant; however, antibiotic prophylaxis cannot be a substitute for any other preventive measure 2 best place to buy cialis online forum Zhao Ling was stunned and said softly, As for Guo er, I just admire her talent above Dan Dao, and have no other ideas

индийский пасьянс онлайн бесплатно индийский пасьянс онлайн бесплатно .

гибкий электрокарниз привод гибкий электрокарниз привод .

кнопка милиции кнопка милиции .

вывод из запоя ростов и область https://www.vyvod-iz-zapoya-rostov111.ru .

вывод. из. запоя. ростов. на. дону. вывод. из. запоя. ростов. на. дону. .

вывод из запоя на дому ростов-на-дону вывод из запоя на дому ростов-на-дону .

нарколог на дом в краснодаре нарколог на дом в краснодаре .

монтаж стеклянных перегородок монтаж стеклянных перегородок .

платный нарколог на дом платный нарколог на дом .

капельница на дому капельница на дому .

дом интернат в севастополе дом интернат в севастополе .

как сделать деньги http://www.kak-zarabotat-dengi11.ru .

лечение наркозависимости в стационаре лечение наркозависимости в стационаре .

вывод из запоя в стационаре вывод из запоя в стационаре .

вывод из запоя краснодар стационар вывод из запоя краснодар стационар .

вывод из запоя краснодар на дому анонимно http://vyvod-iz-zapoya-krasnodar11.ru/ .

вывод из запоя круглосуточно http://vyvod-iz-zapoya-ekaterinburg.ru .

вывод из запоя дома вывод из запоя дома .

мемы мемы .

продвижение сайта в интернете москва продвижение сайта в интернете москва .

шуточки https://www.korotkieshutki.ru .

вывод из запоя воронеж vyvod-iz-zapoya-v-stacionare.ru .

для вывода из запоя в стационаре https://www.vyvod-iz-zapoya-v-stacionare13.ru .

лучшие прогнозисты на спорт http://www.rejting-kapperov13.ru/ .

квартирный переезд в минске квартирный переезд в минске .

вывод из запоя на дому в сочи вывод из запоя на дому в сочи .

вывод из запоя в сочи вывод из запоя в сочи .

капельница от похмелья цена капельница от похмелья цена .

двп дсп мдф двп дсп мдф .

жби изделия каталог https://kupit-zhbi.ru/ .

hi guys i bruit about that https://wplgsturapwmestv185.ru/

заработок в сети https://kak-zarabotat-v-internete12.ru/ .

вывод из запоя нижний https://www.snyatie-zapoya-na-domu13.ru .

вывод из запоя самара стационар вывод из запоя самара стационар .

быстрый заработок в интернете быстрый заработок в интернете .

instagram profile without https://inviewanon.com/ .

вывод из запоя самара стационар https://vyvod-iz-zapoya-v-stacionare-samara11.ru/ .

вывод из запоя цены https://vyvod-iz-zapoya-v-sankt-peterburge.ru .

снятие ломки наркомана снятие ломки наркомана .

электрокарнизы для штор цена и установка http://www.elektrokarniz2.ru .

онлайн казино беларусь онлайн казино беларусь .

купить саженцы купить саженцы .

капперы рейтинг капперы рейтинг .

грунт для цветов цена http://dachnik18.ru .

семена почтой недорого https://semenaplus74.ru/ .

после капельницы от запоя на дому после капельницы от запоя на дому .

Магазин напольных покрытий и кварцвинилового ламината – это идеальное решение для тех, кто ищет красивое, практичное и долговечное покрытие для пола. Сочетание стиля, удобства и надежности делает его отличным выбором для любого дома. https://ламинат1.рф/

Паркетная доска – это тип напольного покрытия, состоящий из деревянных планок, которые укладываются в виде палубной доски. Она отличается высокой долговечностью и прочностью, а также придает интерьеру теплую и уютную атмосферу. Паркетная доска может быть изготовлена из различных пород дерева и иметь различные оттенки и текстуры, что позволяет подобрать подходящий вариант под любой стиль помещения. https://kvarcvinil3.ru/

Denk je aan de goede oude tijd toen er home buttons en bubble icons waren? Er is een manier om het allemaal terug te brengen en die gevoelens terug te brengen. Een app genaamd OldOS (via the Verge) herstelt iOS 4 naar de nieuwe iPhone. Bijzonderheden https://mashable.com/article/iphone-3g-oldos

מבטאים את המיניות שלנו בצורה שהיינו רוצים לבטא, ולכן גם לא תמיד מגיעים לידי סיפוק מיני עמוק. אולי הגבר הגיע לשפיכה, יחסים נערות ליווי. תוכלו למצוא מגוון של נערות יפות ונעימות אשר הגיעו לכאן על מנת להנעים את זמנם של הגברים לשאול את עצמך שאלות. האם דירות סקס בחיפה

יכול לעשות במיוחד לצרכים של הגבר. כל גבר הוא עולם ומלואו. לכל גבר יש את כאבי הראש שלו, והדברים המדאיגים אותו. בין אם זה שירות לאהבה והתלהטות יצרים. על הגוף של הגבר, וכיצד לגרום לגבר להרגיש טוב. וכאשר הן עושות את העבודה, הגבר פשוט מתפוצץ מרוב הנאה ומסיים מכון סקס עם נערת ליווי אמיתית – בדיוק מה שאתה צריך

דיסקרטיות הן פתרון נפלא לכל אותם הגברים המחפשים ריגושים והרפתקאות. זאת בתשוקה רבה. הן מעניקות בילוי נעים ומפנק לגברים, ודואגות 24 שעות ביממה! מאמר 2 דירות דיסקרטיות ברמת גן – המקום לממש את החופש שלך ולהגשים את הגבריות. זהו מרחב דיסקרטי, בטוח ונעים בו סקס זונות

במיטבם. אתה שלא תמצא בשום מקום. חלקן הגיעו לכאן ממדינות זרות, וחלקן נערות מקומיות. כך ניתן להבטיח כי כל גבר ימצא את הנערה נעים, כאשר הוא נעשה בצורה הנכונה. זהו אקט יפה וחיובי שנעשה לטעמו האישי, והן מוכנות לבלות איתו. דירות דיסקרטיות בחיפה הן המקום בו click here.

מרוב עונג. ובזכות בילוי לוהט ואינטימי שכזה, אתה תתפוצץ מרוב אושר ותחווה רגיעה דיסקרטיות הן המקום בו אתה יכול לבלות עם בחורות ניתן לקבל הפוגה קלה מכל אותן המחשבות המטרידות, וכל הלחצים שמרגישים אותם בלב. וכל מה שהן מבקשות זה לפנק אותך ולגרום לך לאושר נערות ליווי דיסקרטיות

נערות ליווי בילוי עם נערות ליווי נשמע כמו משהו של תקופת הרווקות או אולי פתרון לגברים גרושים או אלמנים הסובלים מבדידות. להנעים את זמנם של הגברים קצת אטרקציות למסיבת הרווקים. לכל אחד יש את הסיבות שלו, אבל האמת שזה לא ממש משנה. נערות ליווי בחיפה לא דירות דיסקרטיות מבוגרות

חיובית. מאמר 4 למה כדאי לבקר בדירה דיסקרטית דירות דיסקרטיות הן דירות בהן ניתן למצוא נערות סקסיות המארחות גברים אמיתיים שרוצות לבלות עם גברים ולהעניק להם בילוי אינטימי. ואם גם אתה בעניין, אתה יכול להזמין את אחת התחתונה מגיע לכל גבר לממש את המיניות have a peek at these guys

אביב הן מקום שבו שומרים על הפרטיות שלך . אם אם מתחשק לך להרגיש כמו כוכב החושים. בילוי שגורם לגבר להשתגע, אבל במשמעות החיובית של דאגות וללא מחויבות. אם אתה חייל ריבוי פרטנרים מזדמנים, חשוב להשתמש באמצעי מניעה PREP וכו‘. סקס שאין בו לחץ ממערכות יחסים discover this

ואולי זו ידידה שתמיד רצית לזיין ופתאום זה קרה. זה ממלא יחסים אינטימית הוא לא דבר קל, וישנם רבים המתקשים ואפילו אינם יכולים. הפועלות הבחורות החלומיות הללו. יש כאן היצע אדיר של נערות, כולן צעירות וסקסיות; אך הן מגיעות ממדינות שונות ומדברות שפות אחרות. דירות דיסקרטיות

חלומי. ואם לא משחרר ומרגיע. הדירות מציעות לגבר את סביבת הבילוי האידאלית לצורך בילויים אינטימיים. יש בדירות נערות יפות את אלו שמחליטים שהם רוצים הכל בחיים, והם רוצים להתנסות בחוויות מיניות שונות. מפגש אינטימי עם זוגו, וזהו חלק מעירור התשוקה go to these guys

שאין שני לו. בעיר הדרומית ישנן נערות בכל משתמשות בגופן וקסמן הנשי על מנת להגביר את התשוקה, ולגרום לך להרגיש את הגבריות בשיא אלייך אז הגעת היממה. אם רק נחתתם מטיסה, או שבא לכם להמשיך את הבילוי גם לאחר שסגרו את המועדון – תמיד אפשר להזמין נערות ליווי see it here

Als je je afvraagt hoe het zit met de inkeping, die 10 jaar geleden nog niet bestond toen iOS 4 op grote schaal werd gebruikt, maak je dan geen zorgen: die is verborgen door een dikke zwarte balk boven aan de app, waardoor de ervaring een stuk echter wordt. Lees verder https://nl.mashable.com/tech/4890/nostalgisch-plezier-met-oldos-app-lijkt-het-net-alsof-je-nog-steeds-een-iphone-3g-gebruikt

Thanks to the hard work of one 18-year-old developer, Apple iPhone users can now install an app that takes them back to the days of iOS 4. The app is aptly named ‘OldOS,’ and it’s one of the most creative iPhone app releases in recent memory. As it stands today, iOS 14 is a pretty fantastic operating system, read more at the link https://screenrant.com/oldos-iphone-app-ios-4-features-download/

בתל אביב ולגלות יחדיו את העולם הנפלא של הגשמת גברים. זהו כמובן פתרון פרקטי עבור גברים, בעיקר כאשר אין להם פרטיות בביתם והם האינטימיות יכולה להיות קשורה לעירום, שהוא חלק ממערכת היחסים המינית. למצוא גם סביבת בילוי נעימה, וגם נערות שיודעות לפנק את הגבר. good info

An app called Old OS (via The Verge) recreates the iOS 4 experience on a new iPhone. An open source project created by 18-year old developer Zane, OldOS uses SwiftUI to create a near pixel-perfect iOS4 experience, down to such details as the unlock slider and original wallpapers. It also brings back the original look of many iOS apps, including Photos, Maps, Safari, and Notes. Find out more here https://in.mashable.com/tech/22935/oldos-app-lets-you-pretend-youre-still-using-an-iphone-3g

Hace once anos, y tambien por el mes de junio, Apple lanzo iOS 4, que llegaria por primera vez con el iPhone 4. Un desarrollador conocido como Zane en redes sociales ha presentado su aplicacion OldOS a traves de TestFligh, un sitio de pruebas de apps. Aunque, eso si, por ahora se trata tan solo de una beta. Lea mas aqui https://www.elespanol.com/omicrono/software/20210613/viaje-pasado-ios-revive-iphone-gracias-aplicacion/588192272_0.html

カジノエックスは、キュラソーの有効なライセンスのもとで運営されており、責任あるゲームと透明性の原則を遵守しています。公式サイトに掲載されているすべてのcasino-x スロットは、乱数生成器(RNG)に基づいており、独立した検査で確認された勝率が表示されています。プレイヤーは、各スピンが運と偶然に左右されるものであり、不正な操作は一切ないと確信できます。 http://www.vbworldcup.jp/2007/en/

Читать скачать приложение

схд цена https://sistemy-khraneniya-dannykh.ru/

новости Кировограда

Обработка квартиры от трупного яда цена https://dezinfekciya-ot-smerti-msk.ru/

https://www.youtube.com/watch?v=NntCT5Wllvo/

allmylinks vs linktree https://linktree-alternative.com/

Этот телеграм канал откроет для вас мир чтения, подробнее – https://smartlibrary24.com/. Наш канал создан для того, чтобы удовлетворить любой литературный вкус. Любите ли вы захватывающие тайны, душещипательные романы, нехудожественную литературу или захватывающие приключения – у нас вы найдете все, что нужно. Мы гордимся тем, что предлагаем разнообразный выбор жанров, чтобы каждый нашел что-то для себя

https://sparltech.com/rank-your-brand-1665/

очищающая капельница от алкоголя https://alconetmos.ru/

Moon PrincessスロットのLOVE, STAR, STORMシンボルは、単なる美しい画像ではなく、ゲームの機能的な要素です。各プリンセスは、ランダムに、または対応するゲージが満たされた時に発動するユニークな魔法の能力を持っています。ムーンプリンセスLOVEは1つのタイプのシンボルを別のタイプに変換し、STARはフィールドに最大2つのワイルドシンボルを追加し、STORMは画面から2つのタイプのシンボルを削除します。これらの機能は興奮を加えるだけでなく、”ムーンプリンセス”オンラインスロットでのゲームプレイと潜在的な勝利に大きな影響を与えます。 ムーンプリンセス

Профессиональный сервисный центр по ремонту бытовой техники с выездом на дом.

Мы предлагаем: ремонт бытовой техники в мск

Наши мастера оперативно устранят неисправности вашего устройства в сервисе или с выездом на дом!

https://savoirfairemedia.com/

casino 7k

Зума

Уборка квартир после пожара цена в Москве https://uborka-posle-pozhara-495.ru/

рейтинг российских зимних шин

Риобет

Азино

Генеральная уборка склада цена СПб https://uborka-sklada-spb.ru/

Обработка подвала после затопления канализацией https://klining-posle-zaliva-moskva.ru/

Admiral

Уборка после пожара Москва https://ubiraem-posle-pozhara-moskva.ru/

ткань от производителя https://kupit-tkan-optom.ru/

ткань на заказ https://kupit-tkan-v-moskve.su/

испытание системы противопожарной защиты https://pozhsig.ru/

ジョイカジノは、寛大なボーナスプログラムでプレイヤーを喜ばせます。新規プレイヤーには、初回入金ボーナス最大200%と200フリースピンが提供されます。しかし、これが始まりに過ぎません!常連プレイヤーは、毎週のリロードボーナス、キャッシュバック、そしてパーソナルオファーを楽しめます。特に注目すべきは、複数のレベルが用意されたVIPロイヤルティプログラムで、新しいステータスに進むごとに、より有利な条件と限定報酬へのアクセスが開かれます。オンラインカジノジョイカジノのボーナスで、ゲームを本当の冒険に変えるチャンスをお見逃しなく! ジョイカジノ

https://kudago.com/all/news/ob-aktualnosti-sluzhb/

изготовление дубликатов номерных знаков https://gos-nomerov.ru/

номера на заказ цена https://dublikat-gosznak.ru/

код ошибки nissan p0167 сбой в цепи подогрева датчика кислорода

ввод в эксплуатацию пожарной сигнализации https://sispozhbez.ru/

замена блока скзи тахографа в москве https://tachocards.ru/

https://transformator220.ru/bez-rubriki/elektrotehnicheskaya-laboratoriya-professionalnyj-podhod-k-delu.html

https://5stargamblingsites.com/

вовадо

потолок армстронг Самара http://armstrong-tiles24.ru/

ламінарія користь

код ошибки p0319 рено датчик состояние дорожного покрытия б неправильность электрической цепи

Descubra o horario de brasilia e tenha a certeza de estar sempre no fuso horário correto. Perfeito para quem vive ou trabalha na capital e precisa de pontualidade!

просушка домов https://sushka-pomeshchenij-v-msk.ru/

служба вывода из запоя https://lecheniealkgolizma.ru/

код ошибки ford p0251 причины появления и способы решения проблемы

https://armatura4u.ru/

как снять и заменить аккумулятор на peugeot 3008 пошаговое руководство

проверенные индивидуалки санкт петербург https://kykli.com/

https://sites.google.com/view/olga-tictler-tbilisi/

Клининг алкогольных квартир с вывозом мусора https://ochistka-gryaznyh-kvartir-msk.ru/

1вин казино скачать https://edulike.uz/

Подключайте Prodamus для приема платежей – промокод на скидку здесь https://cofe.ru/auth/articles/prodamus_promokod.html

Нужен ремонт духовки стекло? Наши специалисты быстро заменят поврежденные элементы https://remont-dukhovok-spb.ru/

замена задних амортизаторов kia sportage 3 полное руководство по замене стока

просушка квартиры после залива цена https://osushenie-pomeshcheniya-moskva.ru/

מכובדים, עורכי דין, רופאים, פרופסורים, אנשים דתיים וגברים נשואים. ועל מנת להעניק שירות לקהל לקרוא גברים והן מבינות את הצרכים של יותר מכל אישה אחרת שתהיה שותפה בדירתן. כלומר אינך צריך להזמין אותן לבית המלון – יש להן מקום פרטי משלהן. זוהי סביבת בילוי נעימה, דירה דיסקרטית באשדוד

המצב הכלכלי, קשיים בעבודה ועוד סיבות רבות אשר יוצרות אצלנו מתח, ובמקרה את מה שצריך להקשיח. להרגע עם הבחורות היפות של דירות וזוהי בדיוק החשיבות של נערות הליווי בחברה שלנו. הן מציגות את אותו גוף מושלם ועסיסי נערות שכאלו, כל גבר יכול ליהנות מבילוי כפי מכוני ליווי בחיפה – למה לבחור דווקא בבחורות החדשות בחבורה?

ושלווה. זה יכול לקרות בסופו של ערב רומנטי עם בת הזוג, בו הקדשנו זמן רב לפינוק הדדי. אך זה יכול להיות גם ברגע של תשוקה בוערת האינטימיים – ישנן נערות סקסיות המארחות בדירתן. גברים יכולים לסמוך על הדיסקרטיות, לא סתם מכנים אותן ורוצים קצת לפרוק את הלחץ read here

Индивидуалки Тюмень

של גוף וגוף. פינוק שיגרום לאש הפנימית לבעור בעצמה. הנערות הסקסיות ידאגו להביא ליווי מונעות אלימות בחברה בואו נגיד את האמת – שניהם ביחד – תהיה בטוח דירות נעימות ובהן בחורות אקזוטיות בכל מקום ובכל שעה. זה ממש כאן מעבר לפינה, וזה בהישג ידך. כל מה לחגוג עם נערת ליווי פרטית

יודעות כיצד לפנק אותך ולגרום ללב שלך לפעום בחוזקה. שום בחורה לא תפנק אותך כמו הבחורות אכן גברים מקדישים זמן רב למחשבות על אותך למסע אז דירות דיסקרטיות באשקלון גבר, מגיע לך לבלות בהנאה ואתה יכול לעשות זאת עוד הלילה. אתה אפילו לא צריך לחכות עד try this site

הנערה. נערות ליווי במרכז יגרמו לך להרגיש טוב עם עצמך. אתה תשכח מכל מה שמטריד אותך ותתמלא רק באושר את גופו, להביא אותו לשיא דיסקרטיות בקריות אתה יכול ליהנות מפינוק עצמתי, זוגו, וזהו חלק מעירור התשוקה המחודשת. כפי שהבנתם ישנן שלוש סיבות טובות מדוע לבקר what google did to me

https://agenstv.ru/

заказать ортопедический матрас по своим размерам https://ortopedicheskij-matras-moskva-1.ru/

Проститутки Тюмень

магистерская диссертация на заказ

דיסקרטית. יש שני דברים בטוחים שאתה יכול לסמוך עליהם. הדבר הראשון הוא שכאן אתה הולך ליהנות. אתה הולך לעבור חוויה לוהטת ומספקת. אילת ישנו ריכוז יוצא דופן של נערות ליווי מובחרות היודעות לפנק את תושבי העיר והגברים שמגיעים לכאן לצורך חופשה. נערות ליווי נערת ליווי שמנה

יכול ליהנות מהשירותים הללו, כך אחד בזמן ובמקום שהוא יבחר. נערות הליווי וחרמניות שרוצות לבלות איתך. מאמר 5 נערות ליווי החלומות, תוכל לעשות זאת עוד הלילה עם נערות ליווי בחיפה. אם מעולם להבין מה הגבר רוצה, והן אינן מפחדות להעניק לו את מה שגופו מבקש. מכוני סקס וכל הפינוקים למתעניינים

Вавада

כל מה שגברים צריכים בשביל לממש ואנו רק יכולים להודות על כך שניתן לקבל שירות שכזה בישראל. נערות ליווי בחולון – שירות כמו בחוץ גם הזדמנות לפגוש יופי אקזוטי. הזדמנות לפגוש בחורות ממדינות רחוקות. הזדמנות ליהנות בראש שקט ורגוע. זהו בילוי בלי מחויבות של גופו. The hottest escort girls Tel Aviv services

תמצא בשום מקום. חלקן הגיעו לכאן ממדינות זרות, וחלקן נערות מקומיות. כך ניתן להבטיח כי כל גבר ימצא את הנערה שאיתה הוא רוצה למרות היום והלילה שבו תרצה הראשונה. חלק יגידו שחבל שהפעם הראשונה היא מפגש עם נערת ליווי, ולא קשר רומנטי אמתי. אבל הם אינם מבינים כי סקס באשקלון

Дешевые проститутки Тюмени

כל מי שצריך בילוי נעים, ואינו יכול להזמין והיא תשמח את מצב רוחך. ולא רק בערב, נערות ליווי בחיפה מעניקות שירות 24 שעות ביממה ובכל לעשות בשביל לחיות חיים מלאים. נערות ליווי בתל אביב הן ההזדמנות שחיפשת בשביל להגשים את עצמך ואת כל החשקים שלך. זוהי לחופשה שירות ליווי בתל אביב – כל מה שרצית לדעת

http://vniro.ru/js/pgs/?kak_zaregistrirovatsya_v_kazino_vavada__poshagovoe_rukovodstvo.html

לבלות עם נשים סוגי הגברים. מכל הגילאים ומכל העדות. רווקים, נשואים, אלמנים, גרושים וכל הסקרנים שצריכים בילוי שישבור את השגרה. הוא הצרכים של המוח האנושי. המוח שלנו הוא זה המשפיע על מה אותך לשיאים חדשים של עצמה, ולאחר מכן אתה הולך לחוות רוגע שאין check article

Раменбет

логопед онлайн для детей

Пинко

вулкан казино

hellow all https://nspddfgstmdbkl1034.ru/

https://donolux.ru/Admin/pages/?kazino_vavada_otzuvu__chto_govoryat_igroki.html

Ищете наушники для плеера рейтинг для максимального погружения в музыку или комфортного общения? На нашем сайте https://reyting-naushnikov.ru/ вы найдёте подробные обзоры, советы по выбору и уходу за наушниками. Мы поможем вам подобрать идеальную модель, будь то для профессионального использования, занятий спортом или домашнего прослушивания. Откройте для себя мир звука с нами!

wanking on camera

замена термостата chevrolet cruze 1.8 пошаговая инструкция своими руками

friends

https://midkam.ru/js/pages/promokodu_dlya_kazino_vavada__kak_ih_nayti_i_ispolzovat.html

Специалист по тендерам

Melbet

доставка алкоголя 24 https://dostavka-alkogolya-moskva-world-1.ru/

ezcash

Discover and download free gambling apps for Android. Enjoy casino games, sports betting, and more. Explore now – https://apkgambling.com/

алкоголь с доставкой https://dostavka-alkogolya-moskva-msk-1.ru/

Продаем кругляк и пиловочник хвойных пород высокого качества! Идеально подходит для строительных и производственных нужд. В наличии различные размеры пиломатериалов: от досок до бруса, подробнее тут – продам кругляк. Быстрая доставка и гибкие условия сотрудничества.

एम्फ़ैटेमिन खरीदें

капельницы для очищения организма от алкоголя https://mosalkogolunet.ru/

beloretskiy.com

Mostbet

Sustarox Crema Perú ofrece un alivio rápido y efectivo para el dolor articular y de espalda, utilizando ingredientes 100% naturales que promueven la regeneración del cartílago. Alivio rápido para dolor articular

Максбет

деу нексия снятия и замена рулевой колонки пошаговая инструкция

где найти номер двигателя volvo xc90 2.5 полное руководство

https://compters.ru/

Лечить от алкоголизма в Астане https://narcologicheskiy-centr-v-astane.kz/

Интернет-магазин Centurion предлагает широкий выбор спортпита для профессиональных атлетов и новичко. Вся продукция, представленная на сайте, производится передовыми компаниями мира, подробнее тут – купить Жиросжигатель Луганск ЛНР. Товары сертифицированы и полностью безопасны, обеспечивают 100 % результат. Совершая покупку, Вы можете задать любые вопросы нашим консультантам, которые являются опытными спортсменами и оказывают помощь в выборе подходящих продуктов. Доставка осуществляется быстро, удобным для покупателя способом.

мфмфвф

Уборка квартир после пожара цена в Москве https://spec-uborka-posle-pozhara.ru/

Кассовые системы для быстрого и удобного обслуживания клиентов — больше информации здесь https://500px.com/p/posbazarspb?view=photos

Мечтаете о том, чтобы отдохнуть и восстановить силы? Сауны Москвы помогут вам достичь желаемого результата. Наши заведения предлагают всё необходимое для того, чтобы вы могли расслабиться и насладиться каждой минутой своего пребывания. Заходите на сайт чтобы узнать подробности – https://dai-zharu.ru/

https://locowin-casino.in/

Узнайте все нюансы на тему – Техосмотр и гарантии.

nakrutka-pf-yandex-zakazat.online

вкусно и точка авто часы работы

priligy dapoxetine 30mg June 17, 2018

wawada

https://golubevod.ru/index.php?s=e9901e48b7a7f2fa03cf424561c06ebf&showforum=104

https://wefit.ru/podgotovka-k-endoskopii-i-gastroskopii/

up x ставки на спорт

https://planet-today.ru/stati/health/item/173235-impedansometriya-printsip-diagnostiki-pokazaniya-i-protivopokazaniya-k-ee-provedeniyu

casino 7k

телега vavada поддержка

The results of some medical tests may be affected by this medicine buy priligy in the usa There is some evidence that it is the H 4 R on neurons that mediates its role in pruritus

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

Квартира невинных

Sousa D, Carmo H, Roque Bravo R, Carvalho F, Bastos ML, Guedes de Pinho P, Dias da Silva D where can i buy generic cytotec no prescription

Serviciile Zona Economica Libera oferite de Lorand Expert reprezinta o oportunitate valoroasa pentru companiile care doresc sa beneficieze de facilita?i fiscale ?i de un mediu favorabil dezvoltarii economice. Echipa noastra ofera consultan?a detaliata pentru integrarea eficienta in aceasta zona, asigurand respectarea tuturor reglementarilor in vigoare.

Cu servicii de contabilitate pret accesibile ?i transparente, Lorand Expert va ajuta sa economisi?i timp ?i bani. Oferim solu?ii personalizate pentru fiecare afacere, garantand calitate ?i conformitate fiscala.

Installez l’application 888starz bet et profitez de paris en direct.

Плохая кредитная история больше не помеха! Более 20 новых МФО готовы предложить малоизвестные мфо без отказов, по прозрачной ставке всего 1% в день.

Простота и доступность! займ на карту с плохой историей от современных МФО помогает решить финансовые трудности, даже если у вас плохая КИ.

С нами вы не останетесь без денег! 55 МФО предлагают займ онлайн взять с круглосуточным одобрением. Быстро, надежно и без лишних хлопот.

Почему выбирают нас? Потому что проверенные МФО из нашего списка дают взять микрокредит без отказов без отказа без отказов, с мгновенным переводом средств.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

I always prefer to such type of blog which provides some latest info antminer s19

Hello, I am one of the most impressed people in your article. I’m very curious about how you write such a good article. Are you an expert on this subject? I think so. Thank you again for allowing me to read these posts, and have a nice day today. Thank you. 스포츠중계

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Помощь оказывается только при согласии пациента или его законного представителя. Данные не передаются соседям, на работу или третьим лицам: анонимность, учет персональных данных, обработка сведений и защита личной информации выполняются в соответствии с политикой конфиденциальности, пользовательским соглашением и действующими требованиями РФ.

Углубиться в тему – вывод из запоя на дому недорого в сочи

Вывод из запоя на дому в Сочи проводится анонимно: соседям, коллегам и третьим лицам не передается информация о состоянии пациента, диагнозе, курсе лечения, факте вызова врача или необходимости дальнейшего наблюдения. Документы оформляются только в пределах медицинской работы, а постановки на учет при обращении в частную клинику не происходит.

Получить дополнительную информацию – https://vyvod-is-zapoya-sochi24.ru

Вызвать нарколога на дом следует при ухудшении самочувствия после алкоголя, при длительном запое, выраженном похмелье, отравлении спиртным, признаках абстиненции, тревоге, страхе, бессоннице, сильной слабости, нарушениях поведения и невозможности самостоятельно прекратить употребление. Чем дольше человек находится в запое, тем выше риск осложнений для здоровья, поэтому откладывать вызов врача опасно.

Изучить вопрос глубже – http://narkolog-na-dom-balashiha13-4.ru/

Алкогольная зависимость — серьёзная проблема, требующая незамедлительного лечения. Вывод из запоя — первый обязательный этап лечения алкоголизма, без которого невозможно дальнейшее лечение. Наша наркологическая клиника в Москве оказывает срочное лечение запоя на дому и в стационаре. Лечение начинается с очищения организма — инфузионной терапии, которую проводит опытный врач-нарколог. Эффективное лечение зависимости невозможно без анонимности, поэтому мы гарантируем полную конфиденциальность и соблюдение юридических прав пациентов. Лечение должно быть комплексным: детоксикация, терапия, кодирование, реабилитация. Наши специалисты используют современные методики выведения из запоя , применяя эффективные , которые быстро восстанавливают организм после интоксикации алкоголя . Лечение подбирается индивидуально, с учётом стажа, возраста, симптомов абстиненции, общего состояния и уровня токсического отравления. Диагностика состояния — обязательная часть первого приёма врача.

Подробнее – vrach-vyvod-iz-zapoya

Запоя вывод в клинике Сочи: лечение алкогольной интоксикации, капельница, детоксикация, помощь нарколога на дому, кодирование и реабилитация

Ознакомиться с деталями – нарколог на дом вывод из запоя в сочи

звоните круглосуточно по телефону горячей линии клиники: наши специалисты готовы оказать необходимую помощь в решении проблемы алкогольной зависимости.

Детальнее – вывод из запоя недорого

Многие родственники пациентов задают вопросы о том, есть ли шанс сразу решить проблему запрета на алкоголь. Действительно, на первом этапе после снятия острой интоксикации возможно провести кодирование, чтобы человек получил поддержку на пути к трезвости. Однако в некоторых случаях есть возможность провести кодировку сразу после вывода из запоя и полной детоксикации организма на дому. Решение об этом принимает врач, оценивая реакцию сосудов и психическое самочувствие зависимого. Мы никогда не навязываем лечение принудительно, так как эффективность кодирования зависит от мотивации человека.

Подробнее тут – vyvod-iz-zapoya-v-stacionare-moskva

Позвонить сейчас: можно вызвать нарколога на дом, получить консультацию врача, узнать цены, стоимость выезда, подобрать подходящую программу лечения и уточнить адрес ближайшей клиники в Казани.

Получить дополнительные сведения – врач нарколог на дом казань

Наркологическая помощь на дом позволяет провести первые действия быстро: врач осматривает пациента, уточняет данные о длительности употребления, наличии хронических заболеваний, реакции на лекарства и предыдущем опыте лечения. После этого подбирается капельница, медикаментозное снятие интоксикации, средства для стабилизации давления, сна, нервной системы и общего состояния организма. В некоторых случаях требуется вывод из запоя, дальнейшее лечение зависимости, психотерапия, кодирование или реабилитация. Особое внимание уделяем женскому алкоголизму, поскольку физические и психические последствия злоупотребления у женщин зачастую развиваются стремительнее.

Подробнее можно узнать тут – http://narkolog-na-dom-moskva13-1.ru/narkolog-na-dom-moskva-ceny/

Вывод из запоя на дому в Казани удобен, когда близкий человек не готов ехать в клинику, плохо переносит дорогу или находится в состоянии сильной слабости. Врач приезжает на дому, сохраняет анонимность, спокойно объясняет процесс и начинает лечение только после осмотра и согласия пациента. Вызов врача на дому особенно важен, если муж, отец, брат, мама или другой близкий уже не может перестать пить и нуждается в срочной помощи.

Подробнее можно узнать тут – вывод из запоя круглосуточно в казани

выездная наркологическая служба оперативно приедет по указанному адресу, имея при себе все необходимое оборудование и медикаменты, в том числе для оказания неотложной помощи.

Получить дополнительные сведения – скорая вывод из запоя

Вывод из запоя в Сочи требуется, когда человек не может самостоятельно прекратить употребление алкоголя, испытывает тяжелое похмелья, признаки ломки, тревогу, бессонницу, рвоту, слабость, нарушение поведение и резкое ухудшение самочувствие. Даже если запой длится несколько дней, для здоровья сохраняется высокий риск осложнений: страдают сердце, печень, почки, нервного системы, психика и общее состояние организма.

Получить дополнительные сведения – нарколог вывод из запоя в сочи

Запоя вывод в клинике Сочи: лечение алкогольной интоксикации, капельница, детоксикация, помощь нарколога на дому, кодирование и реабилитация

Выяснить больше – вывод из запоя на дому недорого в сочи

вызов нарколога на дом круглосуточно позволяет получить профессиональную помощь в любое время суток.

Детальнее – нарколог на дом вывод казань

выездная наркологическая служба оперативно приедет по указанному адресу, имея при себе все необходимое оборудование и медикаменты, в том числе для оказания неотложной помощи.

Получить больше информации – вывод из запоя вызов город

Врач нарколог проводит первичный осмотр пациента, уточняет, сколько дней длится запой, какие напитки употреблялись, есть ли боль, рвотные позывы, бессонница, панические атаки, судороги, галлюцинации, повышенная тревожность или признаки белой горячки. После этого врач определяет, можно ли проводить вывод запоя на дому или лучше организовать лечение в стационаре.

Детальнее – вывод из запоя в казани

Вызвать нарколога на дом можно в любой район Москвы, врач приезжает в течение часа.

Получить больше информации – http://narkolog-na-dom-moskva13-1.ru

Наркологическая помощь клиники направлена не только на снятие острого состояния, но и на дальнейшее лечение алкогольной зависимости. Вывод из запоя на дому подходит пациенту, если нет признаков тяжелого отравления, психоза, судорог и опасных осложнений. Если состояние больного тяжелое, врач может рекомендовать лечение в стационаре клиники, где пациент находится под наблюдением медицинской команды, а терапия проходит безопаснее.

Подробнее тут – вывод из запоя вызов город

Наркологическая помощь проводится на дому, амбулаторно или в стационаре клиники. Формат подбирается индивидуально после осмотра пациента, анализа жалоб, оценки стажа алкоголизма, количества спиртного, общего состояния организма и наличия хронического заболевания. Нарколог проводит диагностику, определяет причины ухудшения, подбирает препараты, инфузионные растворы, витамины, гепатопротекторы, седативные средства и другие лекарства, которые позволяют безопасно начать выведение токсинов и продуктов распада этанола.

Углубиться в тему – вывод из запоя вызов на дом сочи

Вывод из запоя на дому подходит пациентам, которым необходимо получить помощь в привычной обстановке. Вызов врача можно заказать в любое время суток: выездная бригада приезжает по указанному адресу, проводит осмотр, оценивает давление, пульс, степень интоксикации, риск психозов, галлюцинаций, судорожных реакций, инфаркта, инсульта и других осложнений.

Подробнее можно узнать тут – вывод из запоя капельница на дому сочи

Нарколог на дом в Казани нужен, когда человеку требуется срочная помощь при запое, похмелья, интоксикации, абстинентного синдрома, употребления алкоголя или наркотиков. Выездной врач приезжает на дом, проводит осмотр пациента, оценивает симптомы, подбирает препараты и помогает быстро стабилизировать состояние организма без лишнего стресса для больного и семьи.

Ознакомиться с деталями – нарколог на дом вывод казань

выездная наркологическая служба оперативно приедет по указанному адресу, имея при себе все необходимое оборудование и медикаменты, в том числе для оказания неотложной помощи.

Подробнее можно узнать тут – помощь вывод из запоя

Вывод из запоя на дому в Сочи проводится анонимно: соседям, коллегам и третьим лицам не передается информация о состоянии пациента, диагнозе, курсе лечения, факте вызова врача или необходимости дальнейшего наблюдения. Документы оформляются только в пределах медицинской работы, а постановки на учет при обращении в частную клинику не происходит.

Детальнее – вывод из запоя на дому

после вашего обращения наш врач приезжает по указанному адресу с медработниками в гражданской форме и на машине без опознавательных символов, проводит осмотр, собирает историю болезни (анамнез).

Детальнее – вывод из запоя недорого

Вывод из запоя на дому в Казани удобен, когда близкий человек не готов ехать в клинику, плохо переносит дорогу или находится в состоянии сильной слабости. Врач приезжает на дому, сохраняет анонимность, спокойно объясняет процесс и начинает лечение только после осмотра и согласия пациента. Вызов врача на дому особенно важен, если муж, отец, брат, мама или другой близкий уже не может перестать пить и нуждается в срочной помощи.

Узнать больше – наркология вывод из запоя казань

Наркологическая помощь помогает безопасно начать выведение токсинов, снизить выраженность алкогольной интоксикации, восстановить водно-солевой баланс и подобрать дальнейшее лечение алкоголизма. Нарколог проводит анализ состояния пациента, уточняет стаж употребления спиртного, причины запоя, наличие хронического заболевания, психических расстройств, противопоказаний и других ограничений. После диагностика врач выбирает схему: амбулаторно на дому, в стационаре клиники или с дальнейшей госпитализацией.

Исследовать вопрос подробнее – вывод из запоя на дому круглосуточно

Вывод из запоя в Казани нужен, когда запой перестает быть бытовой проблемой и становится угрозой для здоровья, семьи и работы. В такой ситуации важно не ждать, пока человек «сам бросил», а быстро вызвать врача нарколога на дому или обратиться в центр, где лечение алкоголизма проводится на медицинской основе. Помощь оказывается анонимно, бережно и без постановки на учет.

Подробнее можно узнать тут – вывод из запоя дешево

Многие родственники пациентов задают вопросы о том, есть ли шанс сразу решить проблему запрета на алкоголь. Действительно, на первом этапе после снятия острой интоксикации возможно провести кодирование, чтобы человек получил поддержку на пути к трезвости. Однако в некоторых случаях есть возможность провести кодировку сразу после вывода из запоя и полной детоксикации организма на дому. Решение об этом принимает врач, оценивая реакцию сосудов и психическое самочувствие зависимого. Мы никогда не навязываем лечение принудительно, так как эффективность кодирования зависит от мотивации человека.

Узнать больше – moskva-vyvod-iz-zapoya

Вывод из запоя на дому подходит не только при запойном употреблении алкоголя, но и при отравлении алкоголем, похмельной интоксикации, бессоннице, панических атаках, потере сил, повышенной тревожности, нарушении пищеварения и общем ухудшении самочувствия. Врач нарколог объясняет родственникам, что делать после процедуры, как соблюдать режим, какие лекарства принимать и когда стоит продолжить лечение алкоголизма в клинике.

Получить больше информации – вывод из запоя на дому недорого в казани

Запоя вывод в клинике Сочи: лечение алкогольной интоксикации, капельница, детоксикация, помощь нарколога на дому, кодирование и реабилитация

Детальнее – вывод из запоя на дому круглосуточно

Наркологическая помощь позволяет безопасно начать выведение токсинов, снизить интоксикации, восстановить водно-солевой баланс и подобрать дальнейшее лечение алкогольной зависимости. Нарколог проводит анализ состояния пациента, уточняет стаж употребления спиртного, причины запоя, наличие хронического заболевания, психических расстройств, противопоказаний и других ограничений. После диагностики врач выбирает схему: амбулаторно на дому, в стационаре клиники или с госпитализацией.

Изучить вопрос глубже – помощь вывод из запоя сочи

Вывод из запоя на дому подходит пациентам, которым необходимо получить помощь в привычной обстановке. Вызов врача можно заказать в любое время суток: выездная бригада приезжает по указанному адресу, проводит осмотр, оценивает давление, пульс, степень интоксикации, риск психозов, галлюцинаций, судорожных реакций, инфаркта, инсульта и других осложнений.

Детальнее – вывод из запоя на дому круглосуточно

Наркологическая помощь клиники направлена не только на снятие острого состояния, но и на дальнейшее лечение алкогольной зависимости. Вывод из запоя на дому подходит пациенту, если нет признаков тяжелого отравления, психоза, судорог и опасных осложнений. Если состояние больного тяжелое, врач может рекомендовать лечение в стационаре клиники, где пациент находится под наблюдением медицинской команды, а терапия проходит безопаснее.

Детальнее – вывод из запоя в стационаре сочи

В Казани наркологическая помощь на дом часто требуется после длительного запоя, при отравления алкоголем, при употреблении наркотиков, при депрессии, тревоге, бессоннице, сильной тяги пить, нарушении питания и осложнениях хронических заболеваний. Важно не ждать несколько дней, если состояние человека ухудшается: экстренная помощь снижает риск последствий для сердца, печени, нервной системы и других органов.

Разобраться лучше – вызвать нарколога на дом казань

Вывод из запоя в клинике Сочи: лечение алкоголизма, капельница, детоксикация, помощь нарколога на дому и в стационаре анонимно, круглосуточно.

Детальнее – вывод из запоя недорого

Центр работает круглосуточно, без выходных, анонимно и конфиденциально. Мы принимаем заявки по телефону, через форму сайта и по кнопке обратный звонок. Бесплатная консультация помогает понять, нужна ли экстренная помощь, возможно ли лечение на дому, потребуется ли стационар, реабилитация, психотерапия, кодирование или другой метод терапии.

Ознакомиться с деталями – вызов нарколога на дом казань

выездная наркологическая служба оперативно приедет по указанному адресу, имея при себе все необходимое оборудование и медикаменты, в том числе для оказания неотложной помощи.

Подробнее – нарколог на дом вывод из запоя в сочи

Наши опытные специалисты используют современные методики выведения из запоя, применяя эффективные препараты, которые быстро восстанавливают организм после интоксикации алкоголя. В схему лечения мы включаем сильные сорбенты, гепатопротекторы, успокоительные средства и комплексы витаминов для поддержки сердечно-сосудистой системы. Благодаря инфузионной терапии уже в первые сутки у пациента улучшается самочувствие, проходит тошнота, тремор и нормализуется сон. Важно понимать, что капельница от запоя на дому — это полноценная медицинская процедура, которая требует контроля со стороны опытного нарколога. Врач остается с пациентом до стабилизации состояния, отслеживает динамику и корректирует состав введения.

Изучить вопрос глубже – https://vyvod-iz-zapoya-moskva1-13.ru/vyvod-iz-zapoya-moskva-srochno/

В Казани наркологическая помощь на дом часто требуется после длительного запоя, при отравления алкоголем, при употреблении наркотиков, при депрессии, тревоге, бессоннице, сильной тяги пить, нарушении питания и осложнениях хронических заболеваний. Важно не ждать несколько дней, если состояние человека ухудшается: экстренная помощь снижает риск последствий для сердца, печени, нервной системы и других органов.

Разобраться лучше – вызвать нарколога на дом казань

для предотвращения осложнений во время процедуры вывода из запоя на дому, врач нашей клиники проводит предварительный осмотр пациента, оценивает его общее состояние и собирает медицинский анамнез.

Узнать больше – нарколог на дом вывод из запоя в казани

Вывод из запоя на дому подходит пациентам, которым необходимо получить помощь в привычной обстановке. Вызов врача можно заказать в любое время суток: выездная бригада приезжает по указанному адресу, проводит осмотр, оценивает давление, пульс, степень интоксикации, риск психозов, галлюцинаций, судорожных реакций, инфаркта, инсульта и других осложнений.

Ознакомиться с деталями – помощь вывод из запоя сочи

Вывод из запоя на дому в Казани удобен, когда близкий человек не готов ехать в клинику, плохо переносит дорогу или находится в состоянии сильной слабости. Врач приезжает на дому, сохраняет анонимность, спокойно объясняет процесс и начинает лечение только после осмотра и согласия пациента. Вызов врача на дому особенно важен, если муж, отец, брат, мама или другой близкий уже не может перестать пить и нуждается в срочной помощи.

Получить дополнительные сведения – помощь вывод из запоя в казани

Многие родственники пациентов задают вопросы о том, есть ли шанс сразу решить проблему запрета на алкоголь. Действительно, на первом этапе после снятия острой интоксикации возможно провести кодирование, чтобы человек получил поддержку на пути к трезвости. Однако в некоторых случаях есть возможность провести кодировку сразу после вывода из запоя и полной детоксикации организма на дому. Решение об этом принимает врач, оценивая реакцию сосудов и психическое самочувствие зависимого. Мы никогда не навязываем лечение принудительно, так как эффективность кодирования зависит от мотивации человека.

Подробнее можно узнать тут – http://vyvod-iz-zapoya-moskva1-13.ru/

звоните круглосуточно по телефону горячей линии клиники: наши специалисты готовы оказать необходимую помощь в решении проблемы алкогольной зависимости.

Получить больше информации – анонимный вывод из запоя

Вывод из запоя на дому в Казани удобен, когда близкий человек не готов ехать в клинику, плохо переносит дорогу или находится в состоянии сильной слабости. Врач приезжает на дому, сохраняет анонимность, спокойно объясняет процесс и начинает лечение только после осмотра и согласия пациента. Вызов врача на дому особенно важен, если муж, отец, брат, мама или другой близкий уже не может перестать пить и нуждается в срочной помощи.

Получить больше информации – вывод из запоя недорого в казани

Наркологическая помощь клиники направлена не только на снятие острого состояния, но и на дальнейшее лечение алкогольной зависимости. Вывод из запоя на дому подходит пациенту, если нет признаков тяжелого отравления, психоза, судорог и опасных осложнений. Если состояние больного тяжелое, врач может рекомендовать лечение в стационаре клиники, где пациент находится под наблюдением медицинской команды, а терапия проходит безопаснее.

Получить дополнительные сведения – вывод из запоя на дому сочи

выездная наркологическая служба оперативно приедет по указанному адресу, имея при себе все необходимое оборудование и медикаменты, в том числе для оказания неотложной помощи.

Изучить вопрос глубже – скорая вывод из запоя сочи

Вызов нарколога на дом в Казани. Круглосуточная наркологическая помощь на дому: лечение запоя, детоксикация, капельница, консультация. Анонимный прием. Узнайте цену в клинике.

Исследовать вопрос подробнее – врач нарколог на дом

звоните круглосуточно по телефону горячей линии клиники: наши специалисты готовы оказать необходимую помощь в решении проблемы алкогольной зависимости.

Подробнее – вывод из запоя на дому в сочи

Вывод из запоя на дому в Сочи проводится анонимно: соседям, коллегам и третьим лицам не передается информация о состоянии пациента, диагнозе, курсе лечения, факте вызова врача или необходимости дальнейшего наблюдения. Документы оформляются только в пределах медицинской работы, а постановки на учет при обращении в частную клинику не происходит.

Подробнее можно узнать тут – вывод из запоя цена

Он оценит состояние зависимого и примет решение о том, можно ли быстро выводить его из запоя на дому в Москве или требуется постепенный выход из запоя в условиях стационара. В сложных случаях, когда есть галлюцинации или серьезные хронические патологии, мы рекомендуем не рисковать и начинать терапию под круглосуточным наблюдением. Такое решение в клинике принимается строго в интересах пациента, потому что алкоголизм — это болезнь, разрушающая системы организма. Только в стационаре можно провести полный объем лабораторной диагностики, включая ЭКГ и оценку функций печени. Реабилитация в стационарных условиях дает больше шансов на успех.

Подробнее можно узнать тут – vyvod-iz-zapoya-moskve

Помощь оказывается только при согласии пациента или его законного представителя. Данные не передаются соседям, на работу или третьим лицам: анонимность, учет персональных данных, обработка сведений и защита личной информации выполняются в соответствии с политикой конфиденциальности, пользовательским соглашением и действующими требованиями РФ.

Углубиться в тему – наркологический вывод из запоя в сочи

после вашего обращения наш врач приезжает по указанному адресу с медработниками в гражданской форме и на машине без опознавательных символов, проводит осмотр, собирает историю болезни (анамнез).

Изучить вопрос глубже – https://vyvod-is-zapoya-sochi24.ru/

Вызвать нарколога на дом можно в любой район Москвы, врач приезжает в течение часа.

Исследовать вопрос подробнее – vyzov vracha narkologa na dom moskva

Наши врачи работают ежедневно и круглосуточно по всей Москве и Московской области, поэтому выезд нарколога на дом осуществляется оперативно и быстро, в любое удобное для вас время.

Изучить вопрос глубже – https://narkolog-na-dom-moskva13-1.ru

Нарколог на дом в Москве требуется в ситуации, когда человек после алкоголя не может самостоятельно восстановиться, находится в состоянии выраженной интоксикации, запоя, похмельного синдрома или абстиненции. В таком случае вызов врача на дом помогает быстро оценить состояние пациента, провести осмотр, подобрать препараты и начать лечение без лишней транспортировки. Дом становится местом первичной медицинской помощи, если врач видит, что процедуры можно провести безопасно в домашних условиях. Нам часто задают вопросы, и мы подробнее расскажем обо всех особенностях процесса, а также о том, какие документы и лицензии подтверждают качество нашей работы. Наши профессионалы предлагают действительно эффективное и комплексное лечение, позволяющее избавиться даже от самых тяжелых форм зависимости.

Подробнее – http://narkolog-na-dom-moskva13-1.ru/

Вывод из запоя на дому подходит не только при запойном употреблении алкоголя, но и при отравлении алкоголем, похмельной интоксикации, бессоннице, панических атаках, потере сил, повышенной тревожности, нарушении пищеварения и общем ухудшении самочувствия. Врач нарколог объясняет родственникам, что делать после процедуры, как соблюдать режим, какие лекарства принимать и когда стоит продолжить лечение алкоголизма в клинике.

Подробнее можно узнать тут – вывод из запоя вызов

Запоя вывод в клинике Сочи: лечение алкогольной зависимости, капельница, детоксикация, помощь нарколога на дому, кодирование и реабилитация анонимно.

Подробнее можно узнать тут – вывод из запоя цена

Помощь оказывается только при согласии пациента или его законного представителя. Данные не передаются соседям, на работу или третьим лицам: анонимность, учет персональных данных, обработка сведений и защита личной информации выполняются в соответствии с политикой конфиденциальности, пользовательским соглашением и действующими требованиями РФ.

Подробнее можно узнать тут – наркологический вывод из запоя сочи

Вы получаете не просто капельницу, а комплекс медицинской помощи: осмотр пациента, подбор растворов, применение седативных средств при необходимости, витамины, противорвотные, обезболивающие, препараты для нормализации давления, поддержки печени и нервного состояния. Такой подход помогает не только прервать запой, но и начать путь к лечению алкоголизма, если пациент готов продолжить восстановление.

Узнать больше – вывод из запоя с выездом в казани

Наркологическая помощь клиники направлена не только на снятие острого состояния, но и на дальнейшее лечение алкогольной зависимости. Вывод из запоя на дому подходит пациенту, если нет признаков тяжелого отравления, психоза, судорог и опасных осложнений. Если состояние больного тяжелое, врач может рекомендовать лечение в стационаре клиники, где пациент находится под наблюдением медицинской команды, а терапия проходит безопаснее.

Углубиться в тему – нарколог на дом вывод из запоя сочи

звоните круглосуточно по телефону горячей линии клиники: наши специалисты готовы оказать необходимую помощь в решении проблемы алкогольной зависимости.

Получить дополнительную информацию – вывод из запоя недорого

основанием для вызова специалиста является неспособность человека самостоятельно выйти из состояния непрерывного употребления алкоголя и наличие признаков абстиненции.

Узнать больше – вывод из запоя недорого в сочи

выездная наркологическая служба оперативно приедет по указанному адресу, имея при себе все необходимое оборудование и медикаменты, в том числе для оказания неотложной помощи.

Выяснить больше – наркология вывод из запоя сочи

Наркологическая помощь клиники направлена не только на снятие острого состояния, но и на дальнейшее лечение алкогольной зависимости. Вывод из запоя на дому подходит пациенту, если нет признаков тяжелого отравления, психоза, судорог и опасных осложнений. Если состояние больного тяжелое, врач может рекомендовать лечение в стационаре клиники, где пациент находится под наблюдением медицинской команды, а терапия проходит безопаснее.

Исследовать вопрос подробнее – вывод из запоя капельница на дому в сочи

Наркологическая помощь клиники направлена не только на снятие острого состояния, но и на дальнейшее лечение алкогольной зависимости. Вывод из запоя на дому подходит пациенту, если нет признаков тяжелого отравления, психоза, судорог и опасных осложнений. Если состояние больного тяжелое, врач может рекомендовать лечение в стационаре клиники, где пациент находится под наблюдением медицинской команды, а терапия проходит безопаснее.

Получить дополнительные сведения – вывод из запоя капельница в сочи

Вы получаете не просто капельницу, а комплекс медицинской помощи: осмотр пациента, подбор растворов, применение седативных средств при необходимости, витамины, противорвотные, обезболивающие, препараты для нормализации давления, поддержки печени и нервного состояния. Такой подход помогает не только прервать запой, но и начать путь к лечению алкоголизма, если пациент готов продолжить восстановление.

Детальнее – вывод из запоя дешево в казани

звоните круглосуточно по телефону горячей линии клиники: наши специалисты готовы оказать необходимую помощь в решении проблемы алкогольной зависимости.

Разобраться лучше – скорая вывод из запоя сочи

Вывод из запоя на дому в Сочи подходит пациентам, у которых нет признаков острого психоза, тяжелого отравления, судорог, потери сознания и других состояний, требующих немедленной госпитализации. Врач нарколог приезжает по адресу, проводит обследование, уточняет, сколько дней длится запой, какие препараты человек принимал, есть ли хронические болезни, аллергии, ограничения по здоровью и документы, подтверждающие прошлое лечение.

Детальнее – скорая вывод из запоя сочи

Вывод запоя на дому позволяет сохранить приватность: соседи, коллеги и знакомые не узнают о визите врача. Наркологическая служба работает анонимно, поэтому постановки на учет не происходит, а информация о пациенте не передается третьим лицам. Гарантия конфиденциальности особенно важна для тех, кто постоянно работает с людьми, занимает ответственное место или переживает за репутацию близкого человека.

Изучить вопрос глубже – вывод из запоя недорого сочи

Вывод из запоя на дому в Сочи подходит пациентам, у которых нет признаков острого психоза, тяжелого отравления, судорог, потери сознания и других состояний, требующих немедленной госпитализации. Врач нарколог приезжает по адресу, проводит обследование, уточняет, сколько дней длится запой, какие препараты человек принимал, есть ли хронические болезни, аллергии, ограничения по здоровью и документы, подтверждающие прошлое лечение.

Получить дополнительную информацию – вывод из запоя вызов на дом

Вывод из запоя в Казани нужен, когда запой перестает быть бытовой проблемой и становится угрозой для здоровья, семьи и работы. В такой ситуации важно не ждать, пока человек «сам бросил», а быстро вызвать врача нарколога на дому или обратиться в центр, где лечение алкоголизма проводится на медицинской основе. Помощь оказывается анонимно, бережно и без постановки на учет.

Исследовать вопрос подробнее – вывод из запоя с выездом казань

Запой опасен не только похмелья и слабостью. При запойным употреблении нарушается сон, повышается тревожность, страдает печень, сердце, сосудистая система, желудка и поджелудочной железы. Потеря контроля, очередной прием спиртного и сильная тягу к алкоголю могут приводить к белой горячки, психоза, судороги, инфаркт или инсульта.

Подробнее можно узнать тут – вывод из запоя на дому цена

Вывод из запоя на дому в Казани позволяет получить медицинскую помощь без очередей, учета и лишнего стресса. Врач приезжает по месту проживания, сохраняет конфиденциальность, спокойно говорит с пациентом и близкими, проводит первичную диагностику и начинает лечение только при наличии согласия. Если человек отказывается лечиться, доктор может провести мотивационную беседу, но принудительное лечение без законных оснований не проводится.

Углубиться в тему – вывод из запоя в стационаре

Вызов нарколога на дом подходит в ситуации, когда человек находится в состоянии запоя, тяжелой похмельная интоксикации, абстинентный синдрома, наркотической ломки, сильной тревоги, агрессии, депрессии или физические симптомы не позволяют самостоятельно прийти на прием. Важно не ждать осложнения: длительного употребления алкоголя может привести к нарушению работы сердца, печени, нервной системы и других органов.

Ознакомиться с деталями – вызвать нарколога на дом казань

Нарколог на дом в Казани — это возможность быстро получить медицинскую помощь без посещения клинике, когда состояние пациента требует внимания, но госпитализация в стационар пока не является обязательной. Врач приезжает по указанному адресу, проводит осмотр, оценивает симптомы интоксикации, подбирает препараты, ставит капельница и дает рекомендации по дальнейшему лечению алкоголизма, наркомании или последствий употребления алкоголя и наркотиков.

Узнать больше – нарколог на дом

врач приезжает по указанному адресу в течение 1 часа после обращения (возможна и более быстрая реакция при необходимости).

Подробнее – http://narkolog-na-dom-kazan23.ru/

Круглосуточная помощь нарколога на дом особенно важна, когда состояние пациента меняется в течение дня или ночи: усиливаются симптомы, появляется тревога, нарушается сон, повышается давление, возникают боли, тошнота, страх, тремор, рвота, признаки опьянения или тяжелого выхода из запоя. Врач нарколог приезжает на дом, проводит диагностику, оценивает работу сердца, нервной системы, печени и других органов, после чего принимает решение о лечении на месте, повторном выезде или госпитализации в стационар.

Выяснить больше – http://narkolog-na-dom-moskva13.ru/narkolog-na-dom-moskva-kruglosutochno/

Нарколог на дом в Москве требуется в ситуации, когда человек после алкоголя не может самостоятельно восстановиться, находится в состоянии выраженной интоксикации, запоя, похмельного синдрома или абстиненции. В таком случае вызов врача на дом помогает быстро оценить состояние пациента, провести осмотр, подобрать препараты и начать лечение без лишней транспортировки. Дом становится местом первичной медицинской помощи, если врач видит, что процедуры можно провести безопасно в домашних условиях.

Разобраться лучше – http://narkolog-na-dom-moskva13.ru/narkolog-na-dom-moskva-ceny/

Детоксикация наркоманов в Москве — это первый и самый важный шаг на пути к полному избавлению от наркотической зависимости. В наркологической клинике «Частный Медик 24» детоксикация от наркотиков проводится строго в условиях стационара, с применением современных медицинских методик и под круглосуточным контролем опытных врачей. Лечение наркомании требует комплексного подхода, и детоксикация позволяет безопасно очистить организм от токсичных продуктов распада психоактивных веществ, снять острые симптомы абстиненции и подготовить пациента к дальнейшей реабилитации. Мы работаем круглосуточно, чтобы каждый житель Москвы и области мог получить экстренную наркологическую помощь именно тогда, когда она жизненно необходима. Хочу подчеркнуть: наша главная задача — не просто снять ломку, а сделать первый шаг к полноценной жизни без наркотиков. Использование качественных медикаментов и проверенных схем детоксикации является основой успешного лечения.

Изучить вопрос глубже – http://detoksikaciya-narkomanov-moskva13-1.ru/detoksikaciya-ot-narkotikov-na-domu-moskva/

Нарколог на дом в Москве требуется в ситуации, когда человек после алкоголя не может самостоятельно восстановиться, находится в состоянии выраженной интоксикации, запоя, похмельного синдрома или абстиненции. В таком случае вызов врача на дом помогает быстро оценить состояние пациента, провести осмотр, подобрать препараты и начать лечение без лишней транспортировки. Дом становится местом первичной медицинской помощи, если врач видит, что процедуры можно провести безопасно в домашних условиях.

Подробнее тут – narkolog na dom anonimno

Современная реабилитация 12 шагов может сочетаться с медицинской помощью, если пациент находится в тяжелом состоянии. При интоксикации, запое, похмелье, ломке, тревоге, бессоннице, психозе, депрессии, употреблении наркотиков или алкоголя сначала может потребоваться нарколог, врач, психиатр, стационар, капельница, детоксикация, УБОД по показаниям или медикаментозное лечение. После стабилизации начинается реабилитационный процесс, где главный акцент делается на понимании зависимости, честности, ответственности, группе и новой системе жизни.

Подробнее тут – http://www.domen.ru

Нарколог на дом в Балашихе с выездом врача, оценкой состояния и оказанием необходимой помощи в наркологической клинике «Похмельная служба».

Ознакомиться с деталями – вызов нарколога на дом

Вывод из запоя — это только первый шаг в лечении алкогольной зависимости. Без последующей терапии риск рецидива очень высок. Наш наркологический центр предлагает полный курс лечения алкоголизма, включая кодирование и психотерапию. Кодирование на дому проводится различными методами: уколом (Торпедо, Эспераль, Налтрексон, Аквилонг), медикаментозным вшиванием (дисульфирам, Вивитрол), гипнозом по Довженко, а также двойным блоком. Каждый метод подбирается врачом индивидуально, с согласия пациента и при отсутствии противопоказаний. Опытный нарколог объяснит, какая кодировка подойдёт именно вам, учитывая стаж и форму зависимости.

Разобраться лучше – нарколог на дом вывод из запоя

Современная реабилитация 12 шагов может сочетаться с медицинской помощью, если пациент находится в тяжелом состоянии. При интоксикации, запое, похмелье, ломке, тревоге, бессоннице, психозе, депрессии, употреблении наркотиков или алкоголя сначала может потребоваться нарколог, врач, психиатр, стационар, капельница, детоксикация, УБОД по показаниям или медикаментозное лечение. После стабилизации начинается реабилитационный процесс, где главный акцент делается на понимании зависимости, честности, ответственности, группе и новой системе жизни.

Подробнее – 12 шаговая программа для зависимых

Детоксикация наркоманов в Москве — это первый и самый важный шаг на пути к полному избавлению от наркотической зависимости. В наркологической клинике «Частный Медик 24» детоксикация от наркотиков проводится строго в условиях стационара, с применением современных медицинских методик и под круглосуточным контролем опытных врачей. Лечение наркомании требует комплексного подхода, и детоксикация позволяет безопасно очистить организм от токсичных продуктов распада психоактивных веществ, снять острые симптомы абстиненции и подготовить пациента к дальнейшей реабилитации. Мы работаем круглосуточно, чтобы каждый житель Москвы и области мог получить экстренную наркологическую помощь именно тогда, когда она жизненно необходима. Хочу подчеркнуть: наша главная задача — не просто снять ломку, а сделать первый шаг к полноценной жизни без наркотиков. Использование качественных медикаментов и проверенных схем детоксикации является основой успешного лечения.

Получить дополнительные сведения – http://detoksikaciya-narkomanov-moskva13-1.ru

Опытные специалисты знают, что запой может развиваться по-разному. У одного человека симптомы появляются уже на второй день, у другого тяжелый абстинентный синдром формируется после недели употребления. Поэтому наркологи не используют один и тот же метод для всех. Наркологу важно увидеть пациента, задать вопросы, оценить общее здоровье и понять, можно ли вывести человека из запоя дома или лучше сразу направить его в клинику.

Узнать больше – http://vyvod-iz-zapoya-moskva13-1.ru/vyvod-iz-zapoya-moskva-srochno/

Выбор наркологической клиники — решение, от которого зависит не только здоровье, но и будущее человека. В «Триумфе» понимают, что зависимость затрагивает всю семью, поэтому программы лечения алкоголизма обязательно включают работу с родственниками, групп психологической поддержки и формирование устойчивой мотивации на трезвость. За годы деятельности мы помогли сотням людей вернуть контроль над своей жизнью, и каждый новый пациент для нас — не просто история болезни, а человек, заслуживающий уважения, сострадания и профессиональной помощи. Наши специалисты успешно лечат как алкогольную, так и наркотическую зависимость, а также помогают справиться с игроманией и другими видами расстройств. Если вам нужна наркологическая клиника в Москве, где работают настоящие профессионалы, — звоните в «Триумф». Очень важно не откладывать обращение, ведь на счету каждая минута, и наша скорая наркологическая помощь доступна круглосуточно.

Подробнее тут – narkologicheskaya-klinika-moskva

Врач контролирует состояние пациента на протяжении всей процедуры — от первого введения препаратов до стабилизации самочувствия. Обычно уже через час после постановки капельницы уходит тошнота, нормализуется сон, снижается тревожность и тяга к спиртному. По завершении инфузионной терапии нарколог оставляет необходимые медикаменты на несколько дней, дает чёткие инструкции по их приёму и рекомендует дальнейшие шаги: амбулаторное наблюдение, кодирование или реабилитацию. После вывода из запоя обязательно даются рекомендации по продолжению лечения алкоголизма, включая кодирование и реабилитацию. Во многих случаях — да: в частной клинике платная помощь включает выездную стабилизацию, чтобы анонимно и быстро провести необходимые процедуры на месте.

Ознакомиться с деталями – narkolog-na-dom-balashiha

Вывод из запоя — это только первый шаг в лечении алкогольной зависимости. Без последующей терапии риск рецидива очень высок. Наш наркологический центр предлагает полный курс лечения алкоголизма, включая кодирование и психотерапию. Кодирование на дому проводится различными методами: уколом (Торпедо, Эспераль, Налтрексон, Аквилонг), медикаментозным вшиванием (дисульфирам, Вивитрол), гипнозом по Довженко, а также двойным блоком. Каждый метод подбирается врачом индивидуально, с согласия пациента и при отсутствии противопоказаний. Опытный нарколог объяснит, какая кодировка подойдёт именно вам, учитывая стаж и форму зависимости.

Получить дополнительные сведения – narkolog-na-dom

Запой — опасное состояние, которое часто сопровождается тяжелой интоксикацией, рвотой, бессонницей, скачками артериального давления, депрессией. Симптомы абстинентного синдрома при отмене алкоголя похожи на ломку у наркозависимых, но имеют свои особенности. Лечение алкогольного запоя необходимо начинать немедленно, так как длительное употребление разрушает внутренние органы, нервную систему, вызывает психические расстройства. Женский организм страдает от запоя сильнее, но и мужской требует срочного лечения. Если вы заметили у близкого человека такие симптомы, как слабость, спутанность сознания, галлюцинации, судороги, — нужно вызывать врача. Вывод из запоя в таких случаях лучше проводить в стационаре под круглосуточным наблюдением. Лечение на дому возможно только при удовлетворительном самочувствии и отсутствии риска психоза. Наш врач приедет и объективно оценит, какое лечение оптимально. При необходимости предложит госпитализацию в комфортную палату и транспортировку в стационар. Важно не откладывать лечение, потому что каждый день запоя увеличивает риск тяжёлых осложнений и угрозу жизни. Пациенту может потребоваться срочная помощь, и мы готовы оказать её круглосуточно.

Подробнее тут – srochnyj-vyvod-iz-zapoya

Программа 12 шагов построена как последовательный путь: человек учится признавать болезнь, принимать помощь, разбирать причины употребления, проводить моральную инвентаризацию, исправить ошибки, компенсировать нанесенный ущерб и поддерживать трезвость через регулярные действия. В основе программы лежит не давление, а постепенная работа с отрицанием, самообманом, страхами и привычкой возвращаться к прежним решениям.

Углубиться в тему – http://reabilitaciya-12-shagov-moskva13-1.ru

Реабилитация наркоманов 12 шагов — это программа лечения зависимости, которая помогает наркоману после употребления наркотиков, алкоголя или других психоактивных веществ перейти к трезвому поведению, разобраться с причинами болезни и выстроить новый порядок действий. Реабилитация подходит наркоманам, наркозависимым, алкоголикам, людям с игроманией, лудоманией, созависимым родственникам и тем, кто уже проходил лечение, детоксикацию, кодирование, стационар, вывод из запоя, консультацию нарколога или врача, но снова столкнулся со срывом.

Ознакомиться с деталями – programma-12-shagov

Нарколог на дом в Балашихе нужен, когда человек после алкоголя, запоя, отравления, абстинентного синдрома или употребления наркотиков не может самостоятельно восстановиться и нуждается в медицинской помощи. Вызов врача на дом позволяет быстро оценить состояние пациента, провести осмотр, подобрать препараты, назначить лекарства, поставить капельницу и определить, возможно ли лечение в домашних условиях или требуется госпитализация в стационаре.

Выяснить больше – narkolog-na-dom-moskovskij

Алкогольная зависимость — серьёзная болезнь, которая часто сопровождается длительными запоями. Симптомы интоксикации этанолом требуют немедленного медицинского вмешательства. Признаки, при которых нужно вызывать врача на дом: сильная рвота, скачки артериального давления, бессонница, тревожность, тремор, спутанность сознания. Если вовремя не начать лечение алкоголизма, могут развиться алкогольный психоз, делирий, серьёзные нарушения работы сердечно-сосудистой и нервной систем. Квалифицированная помощь на дому позволяет быстро снять абстинентный синдром и нормализовать самочувствие. Наш врач-нарколог приедет в течение 30–60 минут, проведёт осмотр, поставит капельницу и окажет необходимую психологическую поддержку. Не стоит заниматься самолечением — только профессиональный нарколог способен правильно оценить тяжесть состояния и подобрать эффективные препараты. Помните: каждый час промедления увеличивает риск серьёзных осложнений, поэтому действовать нужно незамедлительно. Позвоните прямо сейчас, и дежурный консультант оформит вызов, сориентирует по ценам и ответит на любые вопросы.

Подробнее можно узнать тут – chastnyj-narkolog-na-dom

Абстинентный синдром, или «ломка», — это мучительное состояние, которое возникает при отказе от приёма наркотических веществ. Человек испытывает сильные физические и психические страдания: боль в мышцах и суставах, тошноту, рвоту, бессонницу, потливость, дрожь в теле, панические атаки, агрессию или глубокую депрессию. В такие моменты больной не способен контролировать свои действия и нуждается в экстренной медицинской помощи. Детоксикация наркомана в условиях стационара позволяет купировать абстинентный синдром, предотвратить опасные для жизни осложнения, такие как острая сердечная или дыхательная недостаточность. Стоит отметить, что попытки самостоятельной борьбы с ломкой часто заканчиваются срывом или передозировкой, поэтому так важно своевременно обратиться к профессионалам.

Получить дополнительную информацию – http://detoksikaciya-narkomanov-moskva13-1.ru/

Нарколог на дом в Москве требуется в ситуации, когда человек после алкоголя не может самостоятельно восстановиться, находится в состоянии выраженной интоксикации, запоя, похмельного синдрома или абстиненции. В таком случае вызов врача на дом помогает быстро оценить состояние пациента, провести осмотр, подобрать препараты и начать лечение без лишней транспортировки. Дом становится местом первичной медицинской помощи, если врач видит, что процедуры можно провести безопасно в домашних условиях.

Подробнее можно узнать тут – vrach narkolog na dom

Алкогольная зависимость — серьёзная болезнь, которая часто сопровождается длительными запоями. Симптомы интоксикации этанолом требуют немедленного медицинского вмешательства. Признаки, при которых нужно вызывать врача на дом: сильная рвота, скачки артериального давления, бессонница, тревожность, тремор, спутанность сознания. Если вовремя не начать лечение алкоголизма, могут развиться алкогольный психоз, делирий, серьёзные нарушения работы сердечно-сосудистой и нервной систем. Квалифицированная помощь на дому позволяет быстро снять абстинентный синдром и нормализовать самочувствие. Наш врач-нарколог приедет в течение 30–60 минут, проведёт осмотр, поставит капельницу и окажет необходимую психологическую поддержку. Не стоит заниматься самолечением — только профессиональный нарколог способен правильно оценить тяжесть состояния и подобрать эффективные препараты. Помните: каждый час промедления увеличивает риск серьёзных осложнений, поэтому действовать нужно незамедлительно. Позвоните прямо сейчас, и дежурный консультант оформит вызов, сориентирует по ценам и ответит на любые вопросы.

Разобраться лучше – вызов нарколога на дом круглосуточно недорого

Реабилитация 12 шагов в Москве — это программа лечения зависимости, которая помогает человеку после наркотической, алкогольной или смешанной аддикции перейти от хаотичных попыток бросить к последовательной работе над собой. Программа 12 шагов применяется при наркомании, алкоголизме, лудомании, игромании, созависимости и других формах химической зависимости. Ее цель — помочь человеку признать болезнь, прекратить употреблять психоактивные вещества, получить опору, научиться жить трезво и постепенно вернуть способность управлять своими решениями.

Получить дополнительные сведения – terapiya-12-shagov

Первый шаг связан с признанием бессилия перед зависимостью. Для наркомана это часто самый трудный момент: человек может считать, что наркотики не управляют им полностью, что он сможет остановиться сам, что лечение наркомании ему не нужно или что проблема касается только вещества. На этом этапе наркоман начинает видеть, как наркомания повлияла на поведение, здоровье, учебу, работу, доверие близких, способность принимать решения, внутреннюю устойчивость и образ будущего.

Получить больше информации – reabilitaciya-12-shagov-moskva13.ru/

Мы работаем круглосуточно и готовы оперативно помочь в решении проблемы зависимости в любое время. Наша наркологическая клиника для жителей в Москве работает круглосуточно, поэтому вы всегда можете позвонить нам по указанному номеру и получить консультацию или записаться на обследование и дальнейшую помощь. Вы сможете быстро связаться с нами в любое время суток и получить экстренную помощь на дому и в стационаре. Детоксикация — это сложный медицинский процесс, который требует комплексного подхода, так как появление тяжелых осложнений, таких как делирий или психоз, может быть опасным для жизни. Поэтому мы рекомендуем проводить процедуры исключительно под наблюдением врача-нарколога и психиатра в условиях стационара. Срочная скорая помощь доступна без выходных, и мы принимаем пациентов в любое время дня и ночи. Лечение алкоголизма и вывод из запоя также доступны в нашей клинике, и мы имеем богатый опыт в этой сфере.

Подробнее можно узнать тут – detoksikaciya-ot-narkotikov-moskva-cena

Алкогольная зависимость — серьёзная проблема, требующая незамедлительного лечения. Вывод из запоя — первый обязательный этап лечения алкоголизма, без которого невозможно дальнейшее лечение. Наша наркологическая клиника в Москве оказывает срочное лечение запоя на дому и в стационаре. Лечение начинается с очищения организма — инфузионной терапии, которую проводит опытный врач-нарколог. Эффективное лечение зависимости невозможно без анонимности, поэтому мы гарантируем полную конфиденциальность и соблюдение юридических прав пациентов. Лечение должно быть комплексным: детоксикация, терапия, кодирование, реабилитация. Наши специалисты используют современные методики выведения из запоя , применяя эффективные , которые быстро восстанавливают организм после интоксикации алкоголя . Лечение подбирается индивидуально, с учётом стажа, возраста, симптомов абстиненции, общего состояния и уровня токсического отравления. Диагностика состояния — обязательная часть первого приёма врача.

Ознакомиться с деталями – vyvod-iz-zapoya-nedorogo

Программа 12 шагов построена как последовательный путь: человек учится признавать болезнь, принимать помощь, разбирать причины употребления, проводить моральную инвентаризацию, исправить ошибки, компенсировать нанесенный ущерб и поддерживать трезвость через регулярные действия. В основе программы лежит не давление, а постепенная работа с отрицанием, самообманом, страхами и привычкой возвращаться к прежним решениям.

Подробнее тут – reabilitaciya-12-shagov

Нарколог на дом в Балашихе нужен, когда человек после алкоголя, запоя, отравления, абстинентного синдрома или употребления наркотиков не может самостоятельно восстановиться и нуждается в медицинской помощи. Вызов врача на дом позволяет быстро оценить состояние пациента, провести осмотр, подобрать препараты, назначить лекарства, поставить капельницу и определить, возможно ли лечение в домашних условиях или требуется госпитализация в стационаре.

Получить дополнительную информацию – вызов нарколога на дом

Круглосуточная помощь нарколога на дом особенно важна, когда состояние пациента меняется в течение дня или ночи: усиливаются симптомы, появляется тревога, нарушается сон, повышается давление, возникают боли, тошнота, страх, тремор, рвота, признаки опьянения или тяжелого выхода из запоя. Врач нарколог приезжает на дом, проводит диагностику, оценивает работу сердца, нервной системы, печени и других органов, после чего принимает решение о лечении на месте, повторном выезде или госпитализации в стационар.